From the Vault - Inflation, PLI and Telecom

Production Linked

Incentives Schemes

PLI Schemes launched in March 2020,

are a cornerstone of the Government’s push for achieving an AtmaNirbhar Bharat.

The idea is to provide support to the sectors, regain dominance in global trade

and be more prepared for the volatilities and shocks in global supply chains as

opposed to the protectionist approach of the pre-1991 era. The objective of the

scheme is to boost domestic manufacturing in sunrise and strategic sectors,

improve cost competitiveness of domestically manufactured goods, enhance domestic

capacity and economies of scale. The scheme is specifically designed to attract

investments in sectors of core competency and cutting-edge technology. The

selection of sectors has been done based on the sectors’ abilities to introduce

latest technology, generate direct and indirect employment by reaching global

scales while increasing competitiveness to ensure penetration of Indian

companies in the global value chains.

This scheme is expected to make

domestic manufacturing globally competitive and will create global champions in

manufacturing. The Government has already committed Rs.1.97 lakh crores, over 5

years starting from 2021-22 in 13 sectors. Recently, PLI in the 14th sector -

drones and drone components has been included with an additional layout of Rs.

120 crores. The initial 13 sectors are Electronic/Technology Products, Medical

devices, Drug intermediaries and APIs, Mobile Manufacturing and Specified

Electronic Components, Pharmaceuticals drugs, Telecom & Networking

Products, Telecommunications, Food Products, White Goods (ACs & LED), High

Efficiency Solar PV Modules, Automobiles & Auto Components, Advance

Chemistry Cell (ACC) Battery, Textile Products: Man Made Fabrics segment and

technical textiles and Specialty Steel.

So far, the 13 initial schemes have been notified and guidelines have been issued where required. The first three schemes notified were for mobile phones and specified electronic components, APIs/Drug intermediates and medical devices. In case of mobile phones and specified electronic components, in the first round, 16 applications worth Rs. 36440 crores were approved and in the second round, 18 applications worth Rs. 483 crores were approved by the competent authority. In case of APIs/drug intermediates and medical devices, 42 applications worth Rs. 4347.26 crore and 13 applications with a committed investment of Rs. 798.93 crores have been approved so far by the competent authority, respectively.

Inflation and Commodity

cycles :

Seasonality in production and

irregular shocks are two important components contributing to the variations in

prices of agriculture commodities, more so in prices of perishable commodities

such as tomato and onion. Seasonality in prices is a result of the varying

pattern of production of these commodities during different months of a year.

On the other hand, shocks often originate from uncertain weather conditions and

other unpredictable events. Distinguishing between these two, however, is

important as policy can be oriented at least towards addressing the more

certain seasonal pattern of price rise.

A time series often has four

components: Trend, Cycle, Seasonal and Irregular. Trend indicates a long-term

rise or fall in prices. A cycle represents a rise or fall in prices that are

not of a fixed frequency such as representing business cycles. Seasonality is

of fixed frequency and occurs at particular points of time during the year.

Seasonality in prices could occur due to the seasonal pattern of production of

agricultural commodities or seasonality in demand such as major festivals.

Irregular component is the remainder in a time series after removing the trend,

cycle and seasonal components. Its magnitude, impact and duration are

unpredictable a priori.

For the current analysis, the seasonal

component of the prices is extracted to identify the seasonality in these

commodities in different months of the year. On the other hand, the irregular

component can be used to identify points of time when various exogenous shocks

have caused spikes in the prices of commodities. The Seasonal-Trend

Decomposition Procedure based on Loess (STL) (Cleveland et al., 1990) was used

for the decomposition. The monthly retail price data at the All-India level

have been taken from Department of Consumer Affairs.

Both seasonal as well as shock

components contribute in the spikes of the tomato and onion prices. Seasonality

in prices resulting from seasonal production patterns require policy attention.

Strategies to incentivize production during lean season should be designed.

Investments in processing of surplus production of tomato, and processing and

storage infrastructure of onion must be promoted. Cutting wastage of the

production, better supply chain management will also help in meeting the

demand.

Government is implementing various

measures to overcome these challenges. The Mission for Integrated Development

of Horticulture (MIDH) envisages holistic development of horticulture and

provides assistance at 50 per cent of total cost of Rs. 1.75 lakh per unit for

low-cost onion storage structure having a capacity of 25 tonne each. Government

also procures onions directly from farmers at farm gate prices for the buffer.

Schemes such as Agricultural Marketing Infrastructure (AMI) for rural godowns

enables small farmers to enhance their holding capacity to sell their produce

at remunerative prices and avoid distress sale. “Operation Greens” for

integrated development of Tomato, Onion and Potato (TOP) value chain.

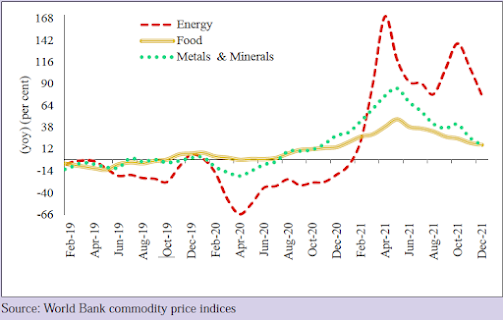

International commodity prices rose

sharply during the second half of 2020 and 2021. Fluctuations have been more in

energy prices. After registering negative growth during the COVID-19 period,

the energy index has recorded triple digit growth in 5 out of 12 months since

January 2021. Food and metals and mineral prices have shown double digit growth

during the current year.

While inflation in food items in India

remained under control because of supply-side management, high global prices of

manufacturing items have had an impact on the domestic prices, especially basic

metals. The rise in demand for vehicles, manufactured goods, and pickup in

construction activities have led to the rise of global aluminium prices. Due to

environmental concerns, China, a major exporter of aluminium, has curtailed its

production.

Copper prices have increased through

the initial months of 2021. The increase in prices is also because of

extraordinary global uptake in consumer goods and demand from China due to its

enhanced investment in infrastructure and construction. Falling inventories and

threats of strikes in Chile and Peru has elevated production risks and created

pressure on copper prices (World Bank, 2021).

The initial surge of iron ore prices

largely reflected the robust demand for steel production in China, leading to

higher iron ore imports. However, recently decline in prices has been observed.

Iron ore supplies have improved in recent months after the earlier weather

disruptions in top exporter Australia and coronavirus outbreaks in number two

shipper Brazil.

Tin prices surged by more than 33 per

cent in the first quarter, reaching a 10-year high in March 2021. Prices were

lifted by buoyant demand for tin solder in consumer electronics, as well as

supply disruptions due to lockdowns in Bolivia, Peru, and Malaysia, voluntary

production cuts in Brazil and Indonesia, and political turmoil in Myanmar.

International cotton prices have been

showing an upward trend since May 2020 and have reached levels higher than

those witnessed in the last ten years. Cotton Index price which stood at

$1.40/kg in April 2020, has sharply risen to $2.79/kg in November 2021, though

it has reduced to $2.65/kg in December 2021. The strengthening of prices of

cotton is owing to the improvement in demand for cotton after COVID-19 related

contraction witnessed in 2020.

Domestic inflation as measured through

WPI of related items have been highly correlated with growth in the

international prices of these commodities. The inflation in domestic aluminium

and copper prices is positively and highly correlated with international

prices.

India is a major producer, consumer,

and exporter of cotton. Therefore, the prices of domestic cotton and

international prices are closely linked. India also imports substantial share

its consumption of edible oils. Any change in international prices of palm oil

gets transmitted into domestic prices as their correlation is around 0.9.

The high inflation rate reported in

the manufactured Group in the WPI is therefore significantly attributable to

“imported inflation” resulting from high prices of imported inputs. High

freight costs and longer delivery times further exacerbated the price pressure

on imported inputs.

Reforms in the

Telecom Sector

Structural

Reforms :

1. Rationalization of Adjusted Gross

Revenue: Non-telecom revenue will be excluded on prospective basis from the

definition of AGR

2. Bank Guarantees (BGs) against

License Fee (LF) have been rationalized. One BGs in different Licensed Service

Areas (LSAs) regions in the country has been allowed.

3. Interest rates rationalized/

Penalties removed: From 1st October, 2021, delayed payments of License Fee

(LF)/Spectrum Usage Charge (SUC) will attract interest rate of SBI’s MCLR plus

2percent instead of MCLR plus 4percent; interest compounded annually instead of

monthly; penalty and interest on penalty removed.

4. For Auctions held henceforth, no

BGs will be required to secure instalment payments.

5. Spectrum Tenure: In future

auctions, tenure of spectrum increased from 20 to 30 years.

6. Surrender of spectrum will be

permitted after 10 years for spectrum acquired in the future auctions.

7. No Spectrum Usage Charge (SUC) for

spectrum acquired in future spectrum auctions.

8. Spectrum sharing encouraged-

additional SUC of 0.5percent for spectrum sharing removed.

9. To encourage investment, 100

percent Foreign Direct Investment (FDI) under automatic route has been

permitted in Telecom Sector with all safeguards applying.

Procedural

Reforms :

10. Auction calendar fixed - Spectrum

auctions to be normally held in the last quarter of every financial year.

11. Ease of doing business promoted -

cumbersome requirement of licenses under Customs Notification for wireless

equipment has been removed. This is replaced with self-declaration.

12. Know Your Customers (KYC) reforms:

Self-KYC (App based) permitted. E-KYC rate revised to only one rupee. Shifting

from prepaid to post-paid and vice-versa does not require fresh KYC.

13. Customer Acquisition Forms (CAF)

in physical form will be replaced by digital storage of data. This is a cost

saving measure as it would allow the Telecom Service Providers (TSPs) to

release several warehouses that was being required to store 300-400 crore paper

CAFs. Further, with this measure, warehouse audit of CAF would also not be

required.

14. Standing Advisory Committee on

Radio Frequency Allocation (SACFA) clearance for telecom towers eased.

Department of Telecommunication will accept data on a portal, based on

self-declaration basis which is to be linked to portals of other Agencies (such

as Civil Aviation).

Addressing

Liquidity requirements of TSPs: The Government approved the following for all

the TSPs:

15. Moratorium/Deferment of up to four

years in annual payments of dues arising out of the AGR judgement, while

protecting the Net Present Value (NPV) of the due amounts.

16. Moratorium/Deferment on due

payments of spectrum purchased in past auctions (excluding the auction of 2021)

for up to four years with NPV protected at the interest rate stipulated in the

respective auctions.

17. Option to the TSPs to pay the

principal and the interest amount arising due to the said moratorium/ deferment

of payment by way of equity.

Number and Composition of internet subscribers